Sign up to our newsletter

Research Coverage

April 2019

Important Information:

This webinar contains information specifically intended for institutional clients, asset consultants, advisers, platforms and researchers, who are professional investors and wholesale clients (as defined in the Corporations Act 2001).

I confirm that I am a professional or wholesale investor as defined by the Corporations Act 2001 and wish to proceed.

1. Why now is a good time to invest in Global SMID.

With the painful Q4 2018 drawdown and subsequent sharp YTD rally in global equity markets behind us, many investors are currently thinking – where to from here?

The unfortunate reality is that we are in the very late stages of what has been an incredibly long bull market in equities. The multitudes of risks in global markets are there for all of us to see and as investors we are staring down a softer global economic backdrop and quite possibly a period of softening earnings.

For investors that were contemplating changes in their global equity portfolios in August / September 2018, but did not act – the YTD rally could prove to be a very timely opportunity to make some changes to sub allocations within global equities.

We would argue that changes to the “Growth” component of a Global equity allocation now could prove to be very pertinent. Simplistically, many large global portfolios “growth exposure” could be categorised into three buckets:

Large Cap Growth has been the stellar performer in most portfolios for several years. The problem now is that Growth stocks have become very expensive – the forward looking P/E ratio of the MSCI World Growth Index is 19.5x which is a 29% premium to the broader market and an 18% premium to its 10 year average. If we do head into a period of slowing earnings, large cap growth stocks are particularly vulnerable to the double whammy of earnings downgrades and multiple compression. The fact that such stocks are so widely held by all forms of active, passive, ETF, quant etc. arguably exacerbates the risk of a drawdown in such names. In summary, now could be a very good time to take profits in what has been an amazing contributor to portfolio returns over several years.

Emerging Markets has arguably also played a ‘growth role’ in most global portfolios for many years. While the long-term performance of EM has been very good, as an asset class it has been susceptible to quite sharp drawdowns (absolute and relative) when markets have retraced. Thanks to a stellar 2017 for EM, over the three years to February 2019 the asset class has outperformed by 2.4% annually. Having said that, the asset class is not without risk and as it becomes increasingly dominated by Chinese equities – the obvious geopolitical risks that we read about daily will continue to weigh on sentiment. The strong YTD rally in emerging market equities has seen their valuations sharply retrace back above their long term averages, even as the earnings outlook softens. It could be argued that investors have been presented with a pertinent profit taking opportunity.

Global Small Caps another ‘growth’ player in global portfolios which has outperformed over a long period of time. Liquidity and Implementation issues seem to be the two interconnected issues that prevent asset allocators from making bigger allocations. In other words, there is seemingly a scarcity of managers who can manage reasonable assets in the Global Small Cap asset class. In our view, much of the problem can be directed at the way the benchmark is constructed. According to the MSCI methodology, the Small Cap index has 4,344 constituents with an average market cap of $1.4bn – which compares with the MSCI World Index average market cap of $24.3bn. We would also make a broader observation that Small Cap stocks – because of the liquidity issues – can in some cases be vulnerable to periods of market volatility.

Global SMID Stocks

Global SMID stocks are probably the least well known / used of the aforementioned growth options used within global portfolios. The two charts on the next page of our report make a strong argument for Global SMID as a viable and attractive sub-allocation within global equity portfolios.

From our point of view – Global SMID stocks should play an important Growth role in Global portfolios. They have less valuation risk than large cap growth, less absolute risk than emerging markets and less liquidity risk than small caps. From a timing perspective, we would argue that an allocation to Global SMID makes sense now. Over the last 5 years as at December 2018, Global SMID has lagged MSCI World by 0.81% annually – which isn’t overly surprising given the mega cap driven bull market we have been through.

In terms of valuation, Global SMID stocks currently trade on a forward P/E of 16.7x which is on par with its 10 year average and at a discount to its 5 year average. They also trade at a material discount to the large cap growth cohort which are on a much more punchy 19.5x.

While it may seem somewhat counterintuitive, we actually feel that SMID earnings as a whole will actually hold up better in what could be a softer earnings period for global equities. The companies - by their very nature tend to be more domestic orientated and therefore less vulnerable to the various geopolitical issues (i.e. Trade wars, Brexit etc.) that can weigh on the mega cap global companies with geographically diversified earnings streams.

In summary, we would argue that investors should seriously consider an allocation to Global SMID stocks now.

2. The case for Global SMID

At a time when global equity strategies are maturing and the search for returns are ever more prevalent after a relatively strong extended period of positive returns, there are a number of arguments that can be made for making a discrete investment allocation to global SMID companies.

The first argument considers Global SMID from an asset allocation perspective. If you believe that growth in sales and earnings are a scarce fundamental commodity that ultimately dictates a company’s share price performance over time, together with stock price inefficiencies of the asset class, then an allocation to Global SMID may add value going forward. Not only does Global SMID hold superior risk-adjusted return characteristics to broad global benchmarks it also offers a strong growth option without a lot of the shortcomings of other global growth asset classes.

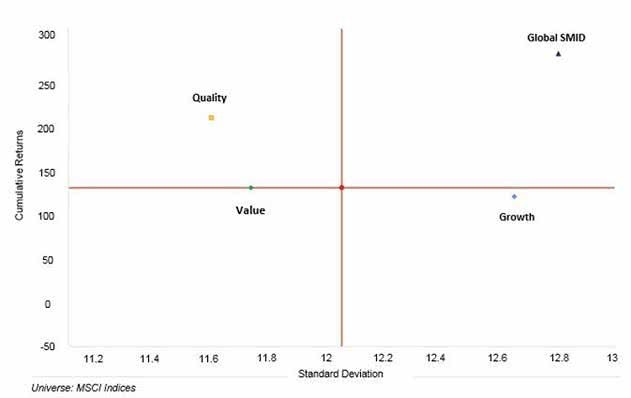

Global SMID generates higher return over Investment Styles Growth, Value and Quality

20 year comparison of Global SMID to Global Value, Growth, Quality and MSCI World

Source: eVestment Alliance: + MSCI Indices is the median of the five Indices shown in the chart. Period is for 20 years ending December 2018, run on a monthly basis. All results are in AUD terms and measured against MSCI World-ND.

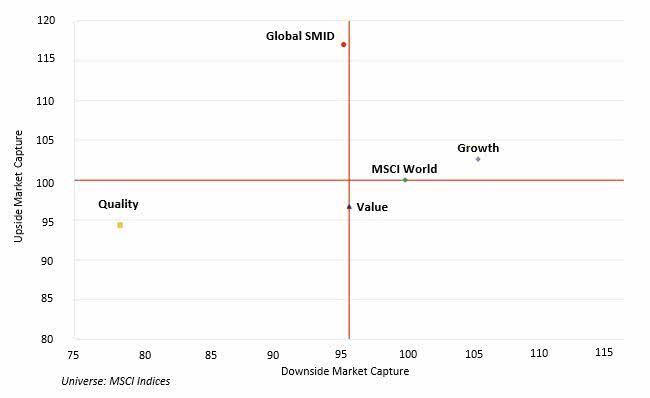

Global SMID offers better downside protection than Value and Growth over 20 years

Source: eVestment Alliance

Asset allocation, specifically when compared to Global Small caps, Global SMID:

To conclude, a discrete investment allocation to Global SMID companies could be seen as a compliment to Global small cap exposure with better liquidity, with the potential growth option. Additionally, as traditional style bucketing is becoming increasingly challenged, greater diversification at a market cap level also provides for positive risk/return characteristics and can further help create great investment opportunities for fundamental /active investors.

3. How does Bell Asset Management find the “hidden gems” amongst global small and mid-cap companies?

Moving down the market cap spectrum to invest in global SMID companies doesn’t mean you have to compromise quality – however, a consistent investment approach is key. We believe a key differentiator for Bell Asset Management is our investment team’s extensive expertise researching and investing in these types of companies for well over a decade.

Bell Asset Management’s approach to global SMID offers much better liquidity than a traditional small caps approach because we only invest in companies with market capitalisation between US$1bn and US$28bn. We also want companies with a track record of high profitability, so additionally, they must have three years of return on equity above 15%. This establishes our starting universe of around 700 companies.

As bottom-up stock pickers, our rigorous and consistent investment approach results in around 150 companies that pass our quality test. We apply a very high bar when analysing whether we consider a company ‘Quality’, which is determined by our investment team undertaking detailed fundamental research and modelling, in conjunction with 500+ company meetings per year. Over the past 16 years, we have accumulated a library of over 10,000 internal research notes and company thesis.

Finally, when constructing the portfolio, we believe that high quality businesses with low levels of debt have the potential not only to provide superior risk-adjusted returns, but may also exhibit defensive characteristics in times of market volatility.

What does Global SMID and Bell Asset Management offer investors?

For more information on our strategies, please visit www.bellasset.com.au

Bell Asset Management is a leading Australian boutique investment manager specialising in global equities. The Melbourne based investment team have been managing global equities of behalf of clients for over 16 years and have a long track record of investing in global small and mid-cap companies. Our clients advise us that one of our key differentiating features is our small and mid-cap bias to global investing.

Investors can access our Global SMID strategy either via a retail fund (Bell Global Emerging Companies Fund ARSN 160 079 541 - BGEC) available via ASX mFund (code: BLM01) and various investment wraps and platforms or, by segregated account.

Disclaimer

Important information: This has been produced by Bell Asset Management Limited (BAM) ABN 84 092 278 647, AFSL 231091. This has been prepared by BAM for information purposes only and does not take into consideration the investment objectives, financial circumstances or needs of any particular recipient – it contains general information only. Before making any investment decision, you should consider your needs and objectives, consult with a licensed financial adviser and obtain a copy of the relevant offering document. No representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein. To the maximum extent permitted by law, none of BAM and its directors, employees or agents accepts any liability for any loss arising, including from negligence, from the use of this document or its contents. This document shall not constitute an offer to sell or a solicitation of an offer to purchase or advice in relation to any securities within or of units in any investment fund or other investment product described herein. Any such offer shall only be made pursuant to an appropriate offer document. This presentation contains forward looking projections that are based on assumptions BAM holds as reasonable, however no guarantee or assurance is given that estimates or targets will be achieved. Past performance is not necessarily indicative of expected future performance.

1. Why now is a good time to invest in Global SMID.

With the painful Q4 2018 drawdown and subsequent sharp YTD rally in global equity markets behind us, many investors are currently thinking – where to from here?

The unfortunate reality is that we are in the very late stages of what has been an incredibly long bull market in equities. The multitudes of risks in global markets are there for all of us to see and as investors we are staring down a softer global economic backdrop and quite possibly a period of softening earnings.

For investors that were contemplating changes in their global equity portfolios in August / September 2018, but did not act – the YTD rally could prove to be a very timely opportunity to make some changes to sub allocations within global equities.

We would argue that changes to the “Growth” component of a Global equity allocation now could prove to be very pertinent. Simplistically, many large global portfolios “growth exposure” could be categorised into three buckets:

Large Cap Growth has been the stellar performer in most portfolios for several years. The problem now is that Growth stocks have become very expensive – the forward looking P/E ratio of the MSCI World Growth Index is 19.5x which is a 29% premium to the broader market and an 18% premium to its 10 year average. If we do head into a period of slowing earnings, large cap growth stocks are particularly vulnerable to the double whammy of earnings downgrades and multiple compression. The fact that such stocks are so widely held by all forms of active, passive, ETF, quant etc. arguably exacerbates the risk of a drawdown in such names. In summary, now could be a very good time to take profits in what has been an amazing contributor to portfolio returns over several years.

Emerging Markets has arguably also played a ‘growth role’ in most global portfolios for many years. While the long-term performance of EM has been very good, as an asset class it has been susceptible to quite sharp drawdowns (absolute and relative) when markets have retraced. Thanks to a stellar 2017 for EM, over the three years to February 2019 the asset class has outperformed by 2.4% annually. Having said that, the asset class is not without risk and as it becomes increasingly dominated by Chinese equities – the obvious geopolitical risks that we read about daily will continue to weigh on sentiment. The strong YTD rally in emerging market equities has seen their valuations sharply retrace back above their long term averages, even as the earnings outlook softens. It could be argued that investors have been presented with a pertinent profit taking opportunity.

Global Small Caps another ‘growth’ player in global portfolios which has outperformed over a long period of time. Liquidity and Implementation issues seem to be the two interconnected issues that prevent asset allocators from making bigger allocations. In other words, there is seemingly a scarcity of managers who can manage reasonable assets in the Global Small Cap asset class. In our view, much of the problem can be directed at the way the benchmark is constructed. According to the MSCI methodology, the Small Cap index has 4,344 constituents with an average market cap of $1.4bn – which compares with the MSCI World Index average market cap of $24.3bn. We would also make a broader observation that Small Cap stocks – because of the liquidity issues – can in some cases be vulnerable to periods of market volatility.

Global SMID Stocks

Global SMID stocks are probably the least well known / used of the aforementioned growth options used within global portfolios. The two charts on the next page of our report make a strong argument for Global SMID as a viable and attractive sub-allocation within global equity portfolios.

From our point of view – Global SMID stocks should play an important Growth role in Global portfolios. They have less valuation risk than large cap growth, less absolute risk than emerging markets and less liquidity risk than small caps. From a timing perspective, we would argue that an allocation to Global SMID makes sense now. Over the last 5 years as at December 2018, Global SMID has lagged MSCI World by 0.81% annually – which isn’t overly surprising given the mega cap driven bull market we have been through.

In terms of valuation, Global SMID stocks currently trade on a forward P/E of 16.7x which is on par with its 10 year average and at a discount to its 5 year average. They also trade at a material discount to the large cap growth cohort which are on a much more punchy 19.5x.

While it may seem somewhat counterintuitive, we actually feel that SMID earnings as a whole will actually hold up better in what could be a softer earnings period for global equities. The companies - by their very nature tend to be more domestic orientated and therefore less vulnerable to the various geopolitical issues (i.e. Trade wars, Brexit etc.) that can weigh on the mega cap global companies with geographically diversified earnings streams.

In summary, we would argue that investors should seriously consider an allocation to Global SMID stocks now.

2. The case for Global SMID

At a time when global equity strategies are maturing and the search for returns are ever more prevalent after a relatively strong extended period of positive returns, there are a number of arguments that can be made for making a discrete investment allocation to global SMID companies.

The first argument considers Global SMID from an asset allocation perspective. If you believe that growth in sales and earnings are a scarce fundamental commodity that ultimately dictates a company’s share price performance over time, together with stock price inefficiencies of the asset class, then an allocation to Global SMID may add value going forward. Not only does Global SMID hold superior risk-adjusted return characteristics to broad global benchmarks it also offers a strong growth option without a lot of the shortcomings of other global growth asset classes.

Global SMID generates higher return over Investment Styles Growth, Value and Quality

20 year comparison of Global SMID to Global Value, Growth, Quality and MSCI World

Source: eVestment Alliance: + MSCI Indices is the median of the five Indices shown in the chart. Period is for 20 years ending December 2018, run on a monthly basis. All results are in AUD terms and measured against MSCI World-ND.

Global SMID offers better downside protection than Value and Growth over 20 years

Source: eVestment Alliance

Asset allocation, specifically when compared to Global Small caps, Global SMID:

To conclude, a discrete investment allocation to Global SMID companies could be seen as a compliment to Global small cap exposure with better liquidity, with the potential growth option. Additionally, as traditional style bucketing is becoming increasingly challenged, greater diversification at a market cap level also provides for positive risk/return characteristics and can further help create great investment opportunities for fundamental /active investors.

3. How does Bell Asset Management find the “hidden gems” amongst global small and mid-cap companies?

Moving down the market cap spectrum to invest in global SMID companies doesn’t mean you have to compromise quality – however, a consistent investment approach is key. We believe a key differentiator for Bell Asset Management is our investment team’s extensive expertise researching and investing in these types of companies for well over a decade.

Bell Asset Management’s approach to global SMID offers much better liquidity than a traditional small caps approach because we only invest in companies with market capitalisation between US$1bn and US$28bn. We also want companies with a track record of high profitability, so additionally, they must have three years of return on equity above 15%. This establishes our starting universe of around 700 companies.

As bottom-up stock pickers, our rigorous and consistent investment approach results in around 150 companies that pass our quality test. We apply a very high bar when analysing whether we consider a company ‘Quality’, which is determined by our investment team undertaking detailed fundamental research and modelling, in conjunction with 500+ company meetings per year. Over the past 16 years, we have accumulated a library of over 10,000 internal research notes and company thesis.

Finally, when constructing the portfolio, we believe that high quality businesses with low levels of debt have the potential not only to provide superior risk-adjusted returns, but may also exhibit defensive characteristics in times of market volatility.

What does Global SMID and Bell Asset Management offer investors?

For more information on our strategies, please visit www.bellasset.com.au

Bell Asset Management is a leading Australian boutique investment manager specialising in global equities. The Melbourne based investment team have been managing global equities of behalf of clients for over 16 years and have a long track record of investing in global small and mid-cap companies. Our clients advise us that one of our key differentiating features is our small and mid-cap bias to global investing.

Investors can access our Global SMID strategy either via a retail fund (Bell Global Emerging Companies Fund ARSN 160 079 541 - BGEC) available via ASX mFund (code: BLM01) and various investment wraps and platforms or, by segregated account.

Disclaimer

Important information: This has been produced by Bell Asset Management Limited (BAM) ABN 84 092 278 647, AFSL 231091. This has been prepared by BAM for information purposes only and does not take into consideration the investment objectives, financial circumstances or needs of any particular recipient – it contains general information only. Before making any investment decision, you should consider your needs and objectives, consult with a licensed financial adviser and obtain a copy of the relevant offering document. No representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein. To the maximum extent permitted by law, none of BAM and its directors, employees or agents accepts any liability for any loss arising, including from negligence, from the use of this document or its contents. This document shall not constitute an offer to sell or a solicitation of an offer to purchase or advice in relation to any securities within or of units in any investment fund or other investment product described herein. Any such offer shall only be made pursuant to an appropriate offer document. This presentation contains forward looking projections that are based on assumptions BAM holds as reasonable, however no guarantee or assurance is given that estimates or targets will be achieved. Past performance is not necessarily indicative of expected future performance.